Lesson 6: Lending and Borrowing

🎧 Lesson Podcast

🎬 Video Overview

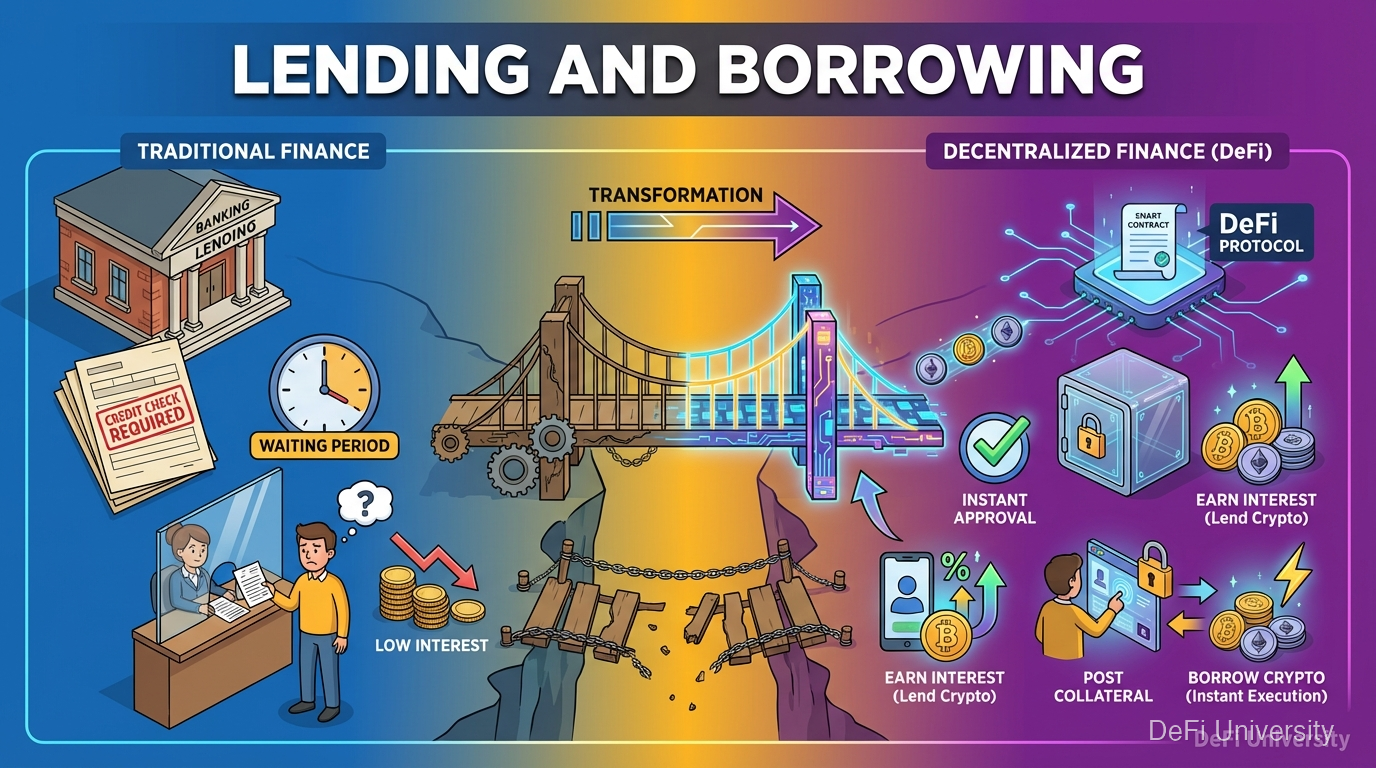

Lesson 6: Lending and Borrowing

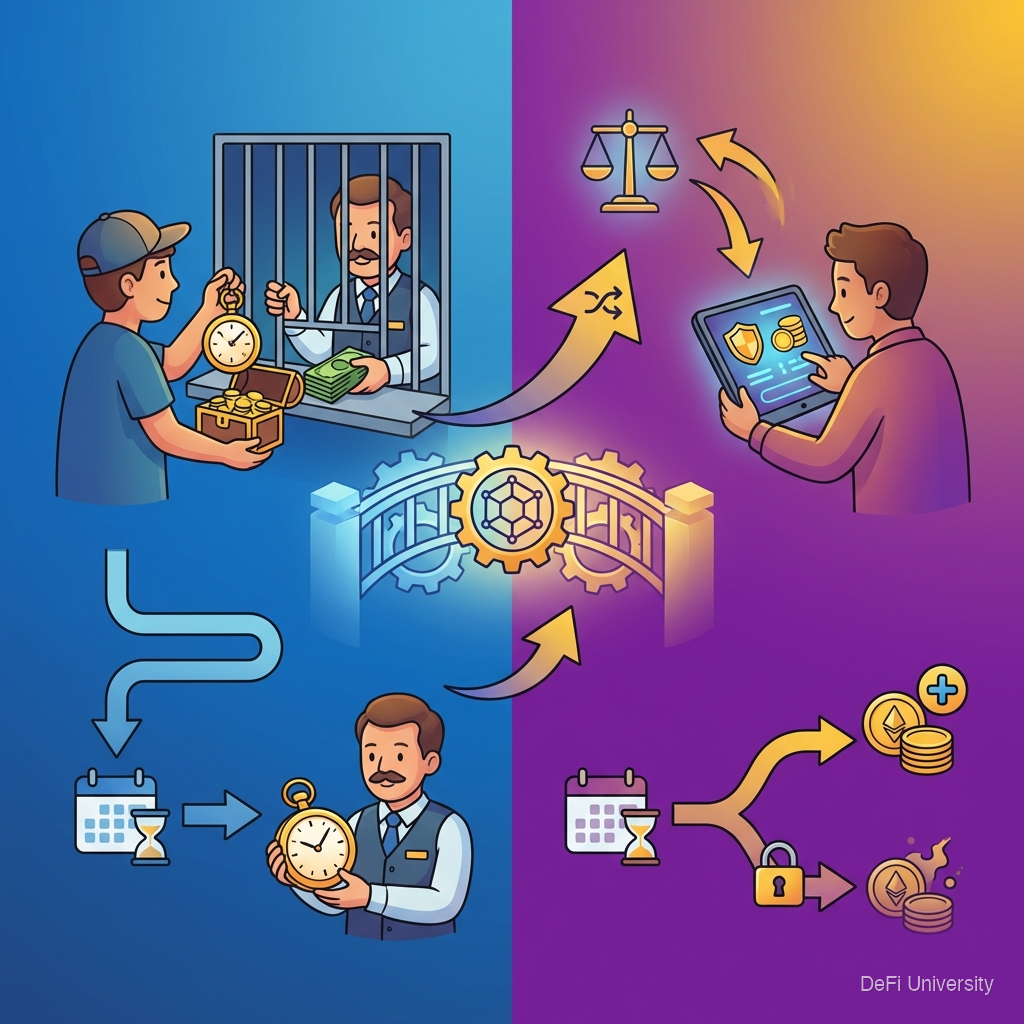

Pawn Shop with Code

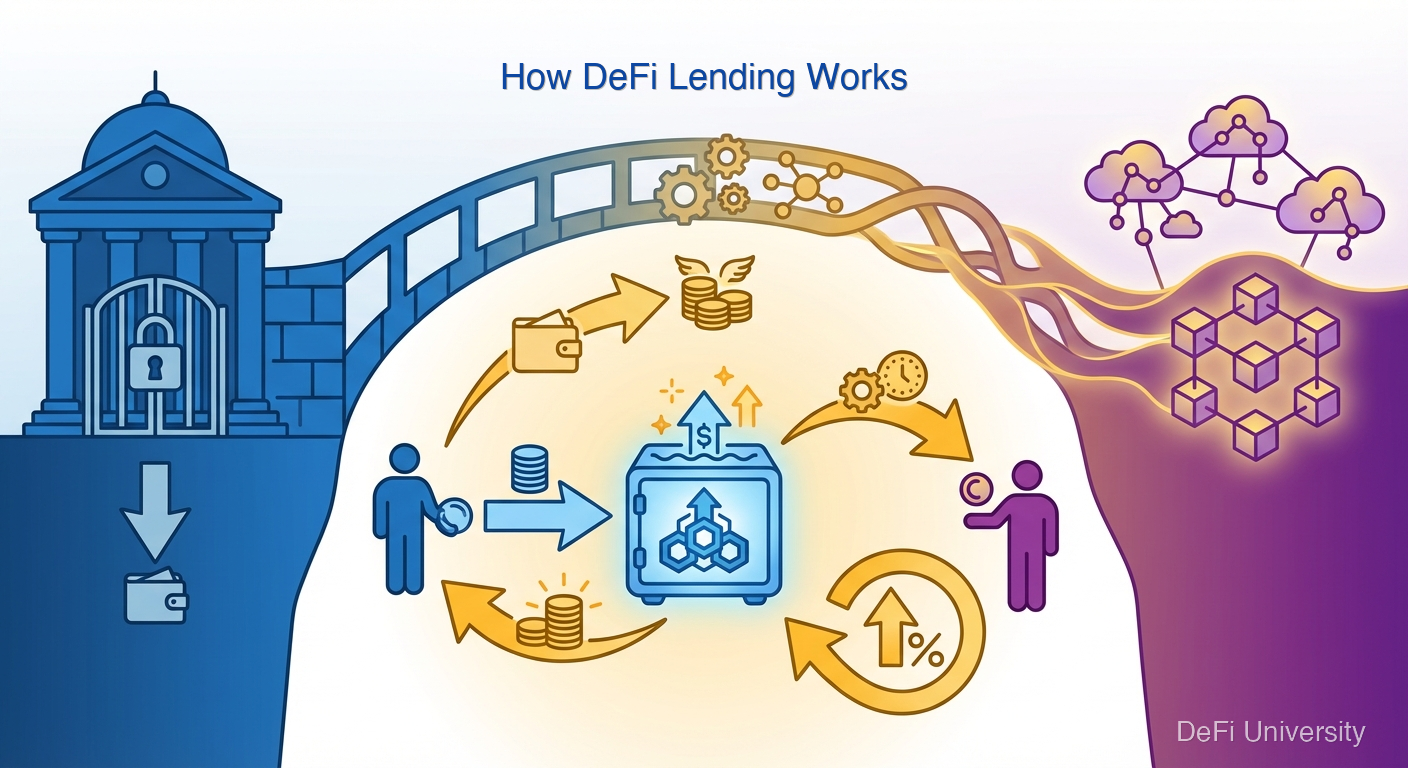

How DeFi Lending Works

The Overcollateralization Requirement

Why Would You Borrow?

Popular Lending Protocols

Risks of DeFi Lending

Key Takeaways

Last updated