Lesson 2: Getting Verified (KYC)

🎧 Lesson Podcast

🎬 Video Overview

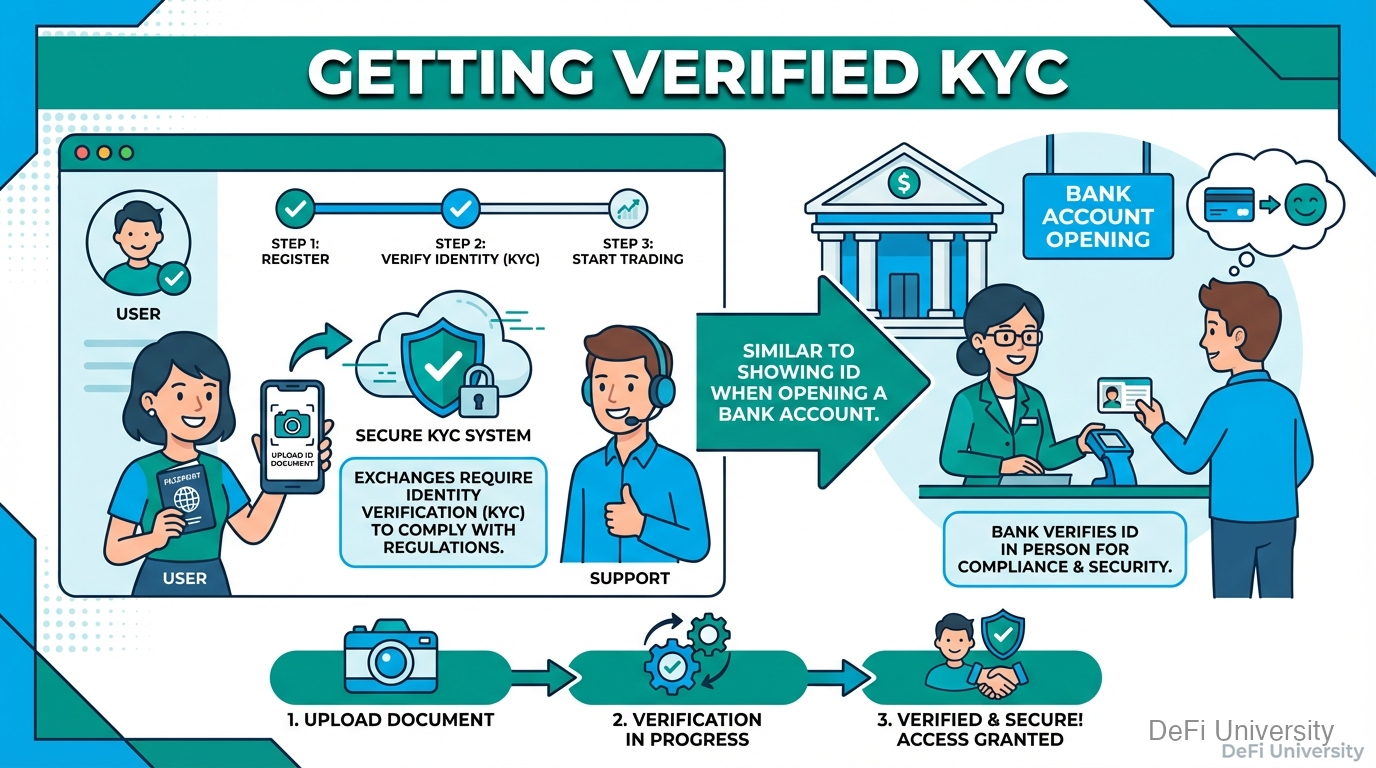

Lesson 2: Getting Verified KYC

Core concept: Most exchanges require identity verification (KYC) to comply with laws—similar to showing ID when opening a bank account.

Showing ID to Open a Bank Account

Remember opening your first bank account? You probably needed:

Government-issued ID

Proof of address (utility bill, lease)

Social Security number

Maybe a parent's signature if you were young

The bank verified who you were before letting you use their services. This wasn't curiosity—it was legal requirement.

Cryptocurrency exchanges face similar requirements. "KYC" (Know Your Customer) and "AML" (Anti-Money Laundering) regulations require them to verify user identities.

What You'll Typically Need

Centralized exchange verification usually requires:

Level 1 (Basic):

Email address

Phone number

Basic personal info (name, birthday)

This might let you: Browse prices, set up account

Level 2 (Standard):

Government ID (passport, driver's license)

Selfie or photo holding ID

Proof of address (sometimes)

This lets you: Buy/sell up to moderate limits

Level 3 (Enhanced):

Additional documentation

Source of funds verification

Higher limits approval

This lets you: Higher transaction limits, full access

Different exchanges have different requirements and limits at each level.

Why KYC Exists

Reasons (good and controversial):

Legal compliance: Governments require financial services to verify customers. Exchanges that don't comply face shutdown.

Prevent financial crimes: Money laundering, terrorist financing, sanctions evasion—KYC helps track these.

Tax reporting: Exchanges often report transaction data to tax authorities.

Fraud prevention: Verified identities help if someone tries to fraudulently access your account.

Controversial aspects:

Privacy concerns—exchanges have your personal data

Excludes people without standard documentation

Data breaches can expose personal information

Some see it as contradicting crypto's permissionless nature

It's a trade-off: regulated exchanges offer easier fiat access and legal protections, but require giving up anonymity.

What to Expect During Verification

Typical process:

Step 1: Create Account Email, password, maybe phone verification.

Step 2: Start Verification Navigate to "verify" or "get verified" section.

Step 3: Personal Information Enter name, address, date of birth, SSN or equivalent.

Step 4: Document Upload Photo of government ID. Both sides. Clear and readable.

Step 5: Selfie/Liveness Check Take a photo or video of yourself. Sometimes holding your ID. Sometimes following prompts (turn head, blink).

Step 6: Wait Verification can take minutes to days depending on exchange volume and your information.

Step 7: Confirmation You'll be notified when verified (or if additional documents needed).

Tips for Smooth Verification

Use clear photos: Good lighting, no blur, all text readable.

Match information exactly: Name should match ID exactly, including middle names if on ID.

Updated documents: Expired IDs are rejected.

Recent address proof: Utility bills or bank statements usually need to be recent (within 90 days).

Be patient: High-demand periods mean longer verification times.

Contact support if stuck: Most exchanges have help for verification issues.

Verification Alternatives

If you want to avoid full KYC:

Decentralized exchanges: DEXs don't require identity verification since you're just connecting your wallet. But you can't buy with fiat directly.

Peer-to-peer platforms: Some platforms connect buyers and sellers directly with varying verification requirements.

Lower limits: Some exchanges offer limited functionality with basic verification.

Bitcoin ATMs: Some have lower verification requirements for small amounts (but often higher fees).

Each alternative has trade-offs in convenience, security, or availability.

Key Takeaways

KYC (Know Your Customer) is identity verification required by law for most exchanges

Similar to bank account opening—government ID, personal info, proof of address

Verification happens in levels—more verification = higher limits

Required for legal/regulatory reasons—fighting financial crimes, tax reporting

Trade-off exists: easier fiat access and protections vs. privacy

Alternatives exist (DEXs, P2P) but with their own trade-offs

Last updated