Lesson 2: Money as a Record-Keeping System

🎧 Lesson Podcast

🎬 Video Overview

Money as a Record-Keeping System

Core concept: Most money today isn't physical—it's entries in databases, a record of who owes what to whom.

The Village Whiteboard

Imagine a small village with 50 people. Everyone knows everyone. When the baker gives the farmer bread, instead of exchanging physical coins, they just write it on a big whiteboard in the town square:

"Farmer owes Baker: 1 loaf of bread worth"

When the farmer later gives the blacksmith some wheat, they update the board:

"Blacksmith owes Farmer: 5 pounds of wheat worth"

At the end of each month, everyone looks at the whiteboard and settles up. The money never physically moved—only the records changed.

This is essentially how money works today, just with computers instead of whiteboards and banks instead of village squares.

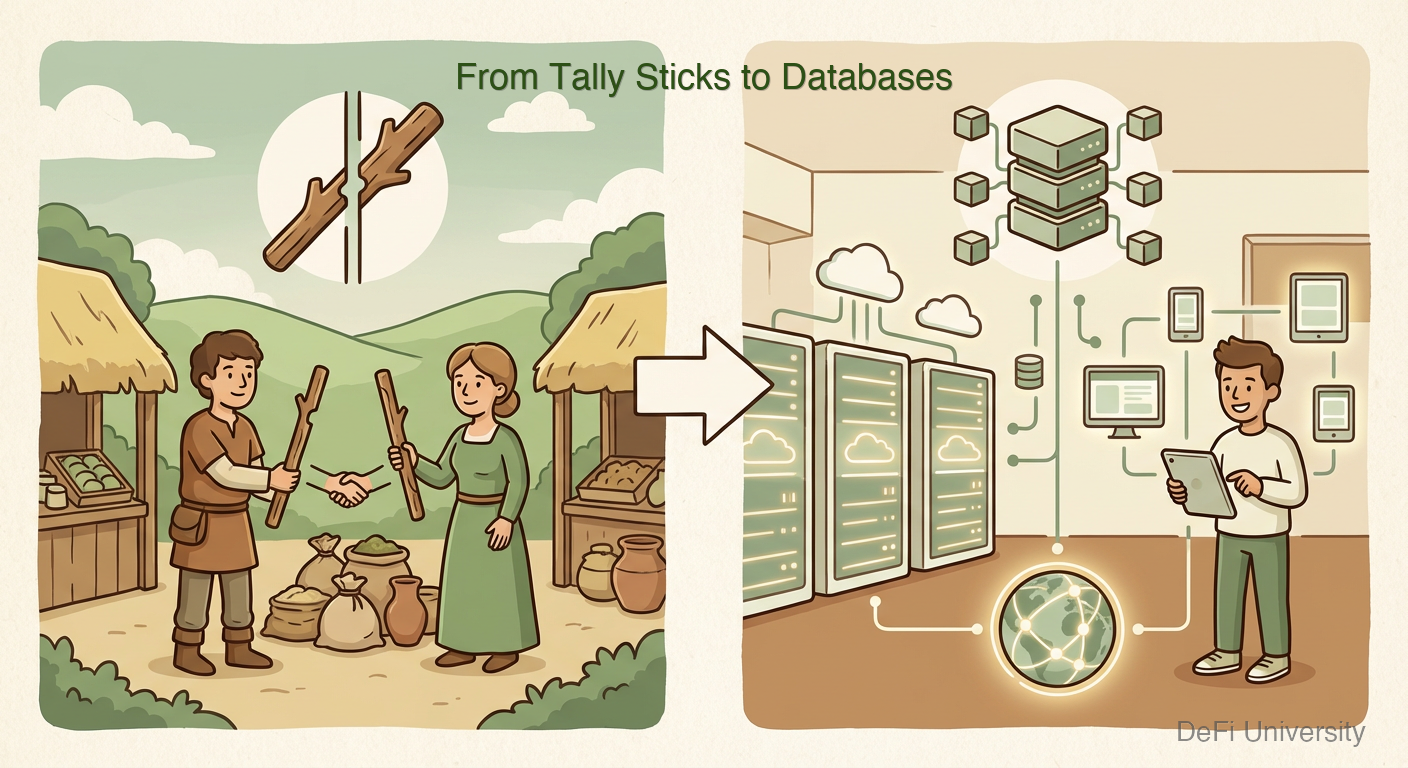

From Tally Sticks to Databases

Humans have been keeping track of debts for thousands of years:

Tally Sticks (Medieval England): A stick was split in half after notches were carved into it. Each party kept half. To verify a debt, you matched the halves together. The king even accepted these as tax payments.

Paper Ledgers (Banks): Banks kept big books recording who deposited what and who owes what. Your "bank balance" was just a number written in their book.

Digital Databases (Today): Now it's all computers. Your paycheck doesn't physically travel—your employer's bank reduces one number and your bank increases another.

The evolution shows a consistent pattern: money became increasingly abstract, moving from physical objects to pure information.

Your Bank Balance Isn't "Money"

Here's something that surprises most people: when you check your bank account and see $5,000, there isn't actually $5,000 sitting in a vault with your name on it.

Your bank balance is a record of what the bank owes you. It's an IOU.

When you "deposit" money, you're actually lending it to the bank. They promise to give it back when you ask (with some limitations). The bank then lends most of that money to other people.

This is why banks can "fail"—if everyone asks for their money at once, the bank doesn't actually have it all. It's spread across loans to other people.

Think of it like a coat check at a fancy restaurant. You give them your coat, they give you a ticket. The ticket represents your coat, but the restaurant might be juggling coats in the back. Usually it works fine. But if there's a fire and everyone wants their coat at once? Problems.

The Ledger Rules Everything

Understanding money as record-keeping helps explain several things:

Why transfers aren't instant: When you send money to a friend, you're not sending anything physical. You're asking your bank to update their records and coordinate with your friend's bank to update theirs. This coordination takes time.

Why you need permission: Since banks control the ledger, they decide who can have an account, who can send money, and when. They're the gatekeepers to the record-keeping system.

Why account freezes work: A government doesn't need to physically take your money. They just tell the bank to change the records—to say you have $0 instead of $5,000.

Why digital is normal: We've been treating money as "information about value" for centuries. Digital money isn't a weird new thing—it's just the latest evolution of the same concept.

The Trust Requirement

For any record-keeping system to work, you need to trust the record keeper. In the village, everyone watched the whiteboard. With banks, you trust that:

They're recording transactions accurately

They won't change the records without permission

They'll actually give you your money when you ask

The government will back them up if things go wrong

This trust is usually well-placed. But it's also a single point of failure. If the record-keeper makes mistakes, gets hacked, or decides to freeze your account, you have limited options.

This is where cryptocurrency enters the story—it's an attempt to create a record-keeping system without needing to trust any single party. But that's for later courses.

Key Takeaways

Most money is just records—entries in ledgers tracking who has what

Your bank balance is an IOU—the bank's promise to pay you, not actual money sitting somewhere

Money evolved from physical to informational over thousands of years

Record-keepers (like banks) have power because they control who can transact

Trust is essential—any monetary system requires trusting someone (or something) to keep accurate records

Last updated