Lesson 12: Your Money, Your Control?

🎧 Lesson Podcast

🎬 Video Overview

Your Money, Your Control?

Core concept: The money in your bank account isn't fully yours in the way cash in your pocket is—you have conditional access that others can restrict.

Renting vs. Owning Your House

When you rent an apartment, you can:

Live there day-to-day

Store your stuff

Have guests over

Make it feel like home

But you can't:

Paint the walls without permission

Change the locks

Stay if you stop paying rent

Refuse entry to the landlord

You have usage rights, not ownership rights. The landlord can set rules, and if things go wrong, they can change your access.

Bank accounts are similar. You have strong usage rights—withdraw, spend, transfer—but the bank retains ultimate control. They can set rules, restrict access, and in extreme cases, lock you out entirely.

Cash in your pocket is different. That you truly own. No one can freeze it remotely or require permission for you to use it.

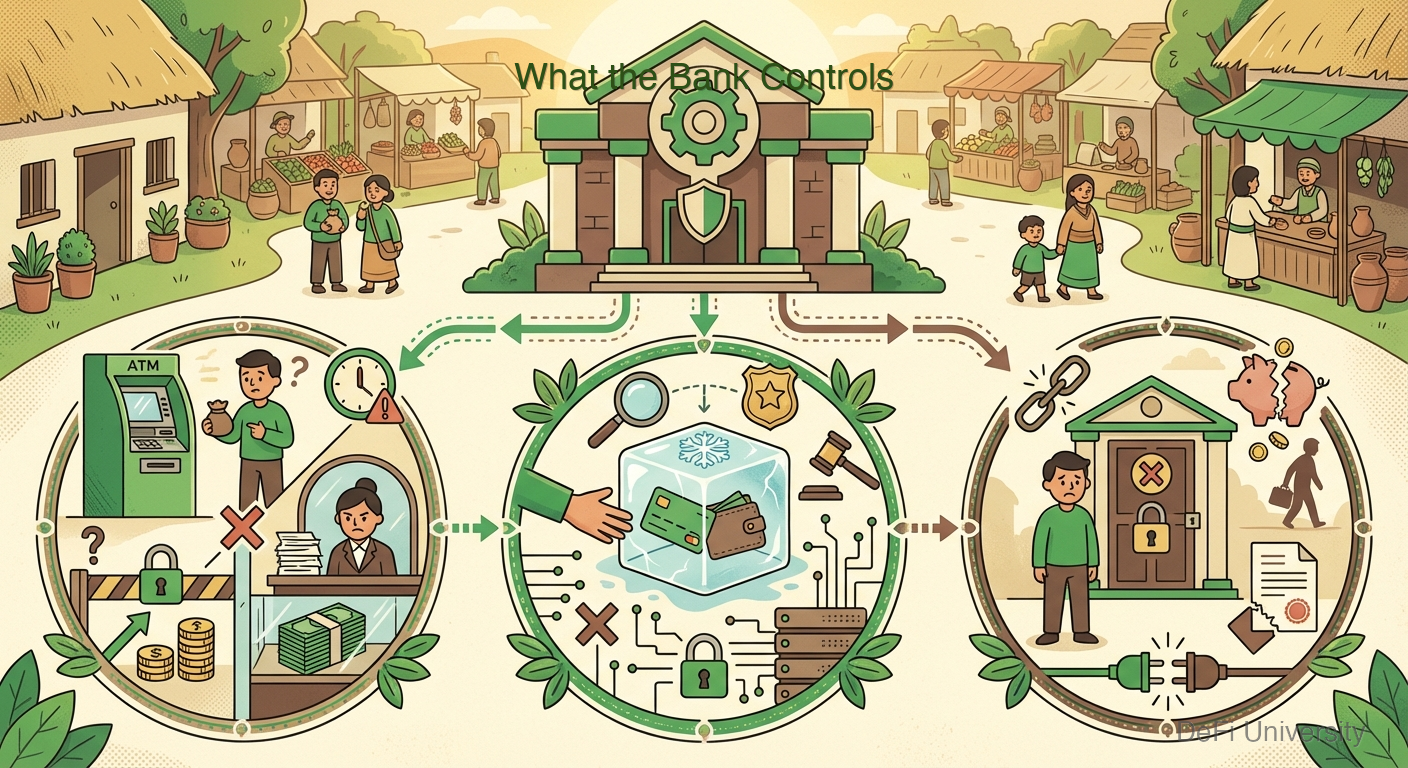

What the Bank Controls

Your bank can:

Set withdrawal limits: Try withdrawing $10,000 in cash and see how many questions you face.

Freeze your account: For fraud investigation, legal orders, or sometimes by mistake.

Close your account: Banks can terminate relationships with little explanation.

Report your activity: Banks must report certain transactions to the government (deposits over $10,000, "suspicious" patterns).

Delay access: Holds on deposits, pending transactions, processing times.

These controls exist for legitimate reasons—fraud prevention, legal compliance, risk management. But they also mean your access is conditional.

When Access Gets Restricted

Account freezes happen more often than you'd think:

Fraud alerts: Unusual spending triggers security holds. Great if it catches actual fraud; frustrating if you're just traveling.

Legal disputes: Divorces, lawsuits, and tax issues can lead to frozen accounts.

Regulatory action: Banks facing pressure about certain industries may restrict customers associated with them.

Algorithmic errors: Automated systems flag accounts incorrectly. Resolution can take weeks.

Political pressure: Controversial but legal activities have seen banking access restricted when institutions face external pressure.

For most people, most of the time, these never become issues. But the possibility exists—and for some, it becomes reality.

Global Perspective

The restrictions in US/European banking are relatively mild. In some countries:

Governments can freeze accounts of political opponents

Hyperinflation makes bank balances worthless before you can withdraw

Capital controls prevent moving money out of the country

Banks simply fail and deposits disappear

For people in stable countries, these sound like edge cases. For the 1.4 billion people without bank access, or billions more with unreliable banking, they're daily realities.

The Spectrum of Control

Different forms of money offer different control levels:

Physical cash: Maximum personal control, but risky to store and transport.

Bank account: High convenience, moderate control—subject to institutional rules.

Payment apps: Similar to banks, sometimes with less protection.

Cryptocurrency in your own wallet: High personal control, but you're responsible for security.

Cryptocurrency on an exchange: Similar to a bank—the exchange controls the keys.

There's no universally "best" option. Each involves trade-offs between convenience, control, security, and access.

Questions Worth Asking

This isn't about fear-mongering against banks. Most people will never face account freezes or access problems. Banks provide valuable services.

But it's worth understanding:

What can interrupt my access to my money?

What recourse do I have if something goes wrong?

Am I comfortable with this level of control trade-off?

For what amount of money might I want different arrangements?

Educated decisions require understanding the actual relationship between you and your money in different systems.

Setting Up for What's Next

This course has covered how money works, how banks function, and how digital payments operate. You now understand:

Money is a trust-based system of record-keeping

Banks are intermediaries that provide services in exchange for fees and control

Digital payments are faster-feeling than actually-faster

Your access to "your" money is conditional

With this foundation, you're ready for the next course: Crypto Fundamentals. There, we'll explore an alternative system where:

Records are kept publicly, not by private banks

No single entity can freeze your account

Transactions settle in minutes, not days

You control your own keys (and your own risks)

Whether that's better depends on your needs and values. But now you have the context to evaluate it properly.

Key Takeaways

Bank accounts give you usage rights, not absolute ownership—like renting vs. owning

Banks can set limits, freeze accounts, close accounts, and report activity—for legitimate and sometimes arbitrary reasons

Access restrictions happen more often than assumed—fraud alerts, legal issues, errors

Different places have different banking reliability—billions face unreliable or no access

Different money forms offer different control trade-offs—cash, banks, crypto each have pros/cons

Understanding control helps you make informed decisions about where to keep money

Last updated