Lesson 6: How Interest Works

🎧 Lesson Podcast

🎬 Video Overview

How Interest Works

Core concept: Interest is the price of using someone else's money—you pay it when you borrow, and you earn it when you lend.

Renting Money

You're familiar with renting things: apartments, cars, tuxedos for prom. You pay money to use something that belongs to someone else, then return it.

Interest is rent for money.

When you borrow $1,000 from a bank, you're renting that money. You use it for whatever you need, then return it with extra—the interest—as payment for the privilege of using it.

When you deposit money in a savings account, you're renting your money to the bank. They use it to lend to others, and they pay you interest as rent.

The difference is that money comes back as numbers, not physical objects. You borrow $1,000, you return $1,050. You deposit $1,000, you get back $1,005.

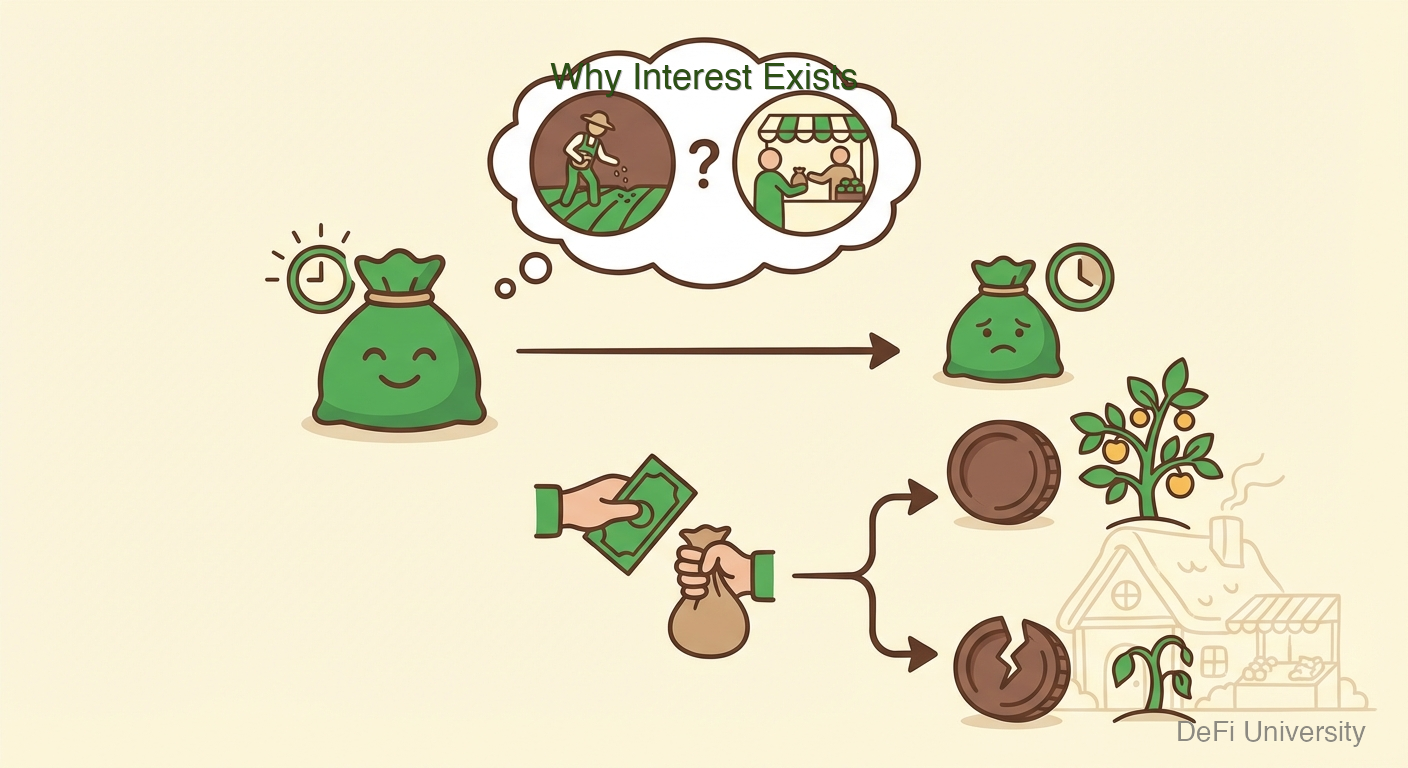

Why Interest Exists

Interest exists because money now is worth more than money later. Here's why:

Opportunity cost: If I lend you $1,000, I can't use it myself. I miss out on whatever I could have done with it—buying something, investing somewhere else, starting a business.

Risk: Maybe you won't pay me back. The possibility of loss needs to be compensated.

Inflation: $1,000 today buys more than $1,000 next year (usually). Lending loses purchasing power over time.

Interest compensates lenders for all three factors. The riskier the borrower, the longer the loan term, and the higher expected inflation—the higher the interest rate.

The Math Made Simple

Interest comes in two flavors:

Simple Interest

You earn interest only on your original amount. If you deposit $1,000 at 5% simple interest for 3 years:

Year 1: $1,000 + $50 = $1,050

Year 2: $1,050 + $50 = $1,100

Year 3: $1,100 + $50 = $1,150

You earned $50 each year on your original $1,000.

Compound Interest

You earn interest on your interest. Same deposit, same rate, but compounded annually:

Year 1: $1,000 + $50 = $1,050

Year 2: $1,050 + $52.50 = $1,102.50

Year 3: $1,102.50 + $55.13 = $1,157.63

The difference seems small, but over long periods, compound interest creates dramatically different outcomes. Over 30 years at 5%:

Simple: $2,500

Compound: $4,322

Albert Einstein (allegedly) called compound interest "the eighth wonder of the world." Whether he actually said it or not, the math is genuinely impressive.

APR vs. APY: The Numbers That Matter

When comparing interest rates, you'll see two terms:

APR (Annual Percentage Rate): The base interest rate, not accounting for compounding. A 12% APR means 1% per month, simple.

APY (Annual Percentage Yield): The actual return after compounding. A 12% APR compounded monthly equals roughly 12.68% APY.

Banks love to show you the APY on savings accounts (bigger number) and the APR on loans (smaller number). Same rate, different presentations. Always compare APY to APY or APR to APR.

Why Your Savings Account Is Losing Money

Here's an uncomfortable truth: most savings accounts pay interest rates below inflation.

If your savings account pays 0.5% APY and inflation is 3%, your money is actually losing 2.5% purchasing power every year. You have more dollars, but those dollars buy less stuff.

Banks profit from this. They pay you 0.5% while lending your money to others at 7-20%. The spread between these rates is their business model—and you're on the wrong side of it.

This dynamic helps explain why people look for alternatives: investments, bonds, or newer options like cryptocurrency yield protocols that sometimes offer higher rates (with different risks).

Interest on Debt: The Flip Side

When you're the borrower, compound interest works against you. Credit card debt is particularly brutal:

Example: $5,000 credit card balance at 20% APR. If you only pay the minimum payment:

You'll pay over $6,000 in interest

It takes 17+ years to pay off

Your $5,000 purchase costs $11,000+

This is why financial advisors always say "pay off high-interest debt first." It's like stopping a leak before filling a bathtub.

Key Takeaways

Interest is rent for money—the price of borrowing or reward for lending

Money now is worth more than money later due to opportunity cost, risk, and inflation

Compound interest earns interest on interest, creating exponential growth (or debt)

APY shows actual returns after compounding; APR shows the base rate

Most savings accounts lose to inflation—you gain dollars but lose purchasing power

Credit card interest compounds against you—small debts become huge over time

Last updated