Lesson 10: How Payment Apps Work

🎧 Lesson Podcast

🎬 Video Overview

How Payment Apps Work

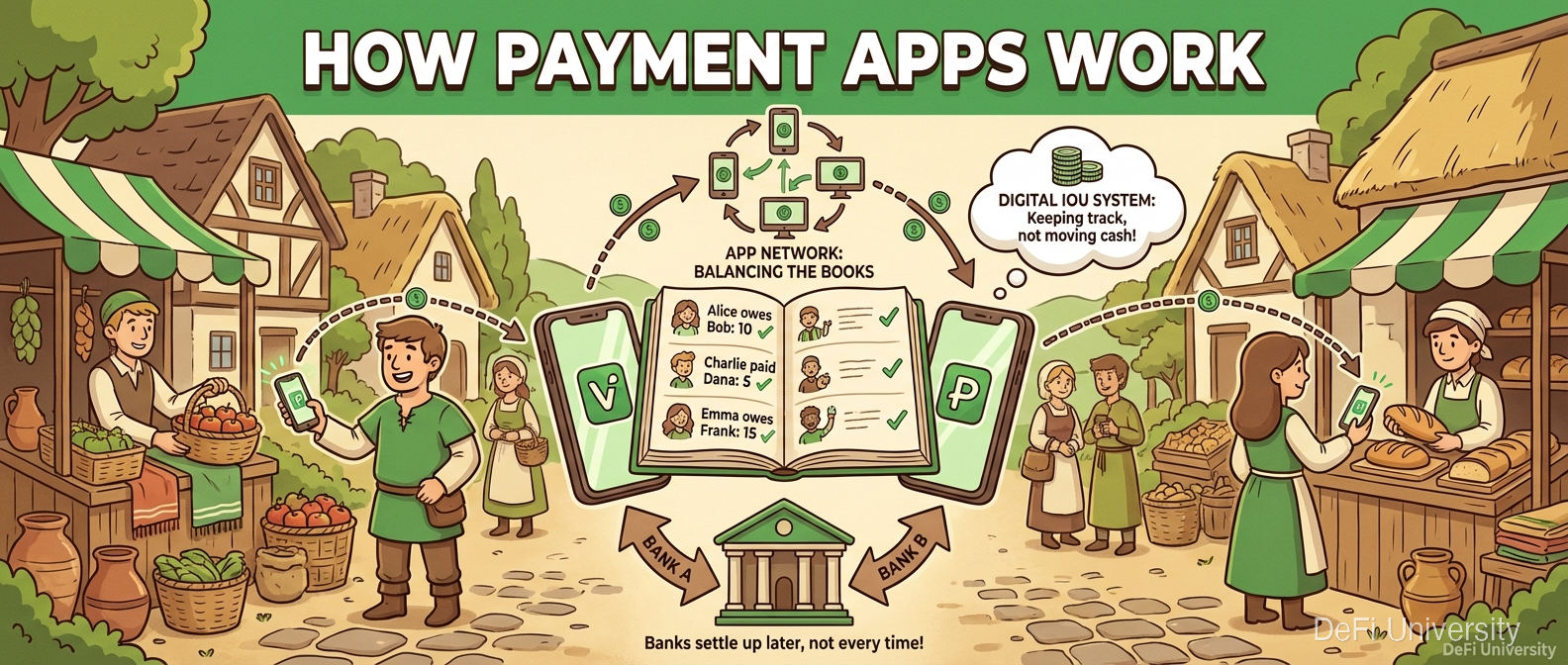

Core concept: Payment apps like Venmo and PayPal are essentially digital IOU systems—they keep track of who owes what without moving actual money every time.

Digital IOUs Between Friends

Remember when you were a kid and your friend bought you a candy bar because you forgot your money? You'd say "I owe you one." No money changed hands, just an understanding between you.

Payment apps work similarly, just at scale.

When you "send" $20 to your friend on Venmo, here's what actually happens: Venmo updates two numbers in their database—your balance goes down $20, your friend's balance goes up $20. No money left Venmo's system.

It's like you're all playing a game where Venmo keeps score. The actual money only moves when someone decides to "cash out" to their regular bank account.

The Different Players

Payment apps come in several flavors:

Closed-Loop Systems (Venmo, PayPal, Cash App)

These apps hold money inside their ecosystem. You can:

Add money from your bank

Send to other users of the same app

Cash out back to your bank

The key: transfers between users are instant because they're just database updates. Money only moves (slowly) when entering or leaving the system.

Bank-Connected Networks (Zelle)

Zelle is different—it's owned by the banks themselves and transfers money directly between bank accounts. Slower than Venmo-to-Venmo but faster than traditional bank transfers.

International Services (Wise, Remitly)

These specialize in currency conversion and international transfers. They often keep balances in multiple countries to make transfers feel faster.

Why It Feels Instant (But Isn't)

When you Venmo someone, it feels instant. But there's a multi-step reality:

Step 1: Database Update (instant) Venmo's computer changes two numbers. Your friend sees the money immediately within the app.

Step 2: You Actually Fund It (1-3 days) If you used your bank account (not Venmo balance), Venmo initiates an ACH transfer to pull money from your bank. This takes 1-3 business days.

Step 3: Your Friend Cashes Out (1-3 days) If your friend wants money in their actual bank account, another 1-3 day transfer.

So that "instant" payment is actually:

Instant if staying in-app

1-3 days for your money to actually fund it

Another 1-3 days for them to access it in their bank

The app's clever design hides this delay. Both of you see money move instantly because Venmo is willing to take the risk while actual settlement happens.

The Business Model

Payment apps make money through:

Instant Transfer Fees: Want money in your bank today instead of 1-3 days? That's 1-1.75% extra.

Merchant Fees: Businesses accepting Venmo/PayPal pay 2-3% per transaction.

Interest on Balances: Money sitting in your Venmo account earns interest—for Venmo, not you.

Credit Products: Many apps now offer loans, credit cards, and "buy now pay later" services.

Data: Your transaction history is valuable for advertising and market research.

The Trust Trade-Off

When you keep money in a payment app, you're trusting that:

The company stays in business

The company doesn't freeze your account

The company's systems don't get hacked

You can withdraw when you want

Unlike bank accounts, most payment app balances aren't FDIC insured. If the company fails, you might not get your money back.

This has happened. Payment companies have frozen accounts for "suspicious activity" (sometimes incorrectly) and users had no recourse. Your money, their rules.

Peer-to-Peer vs. Bank-to-Bank

The apps feel peer-to-peer ("I'm paying my friend") but they're really intermediated:

What you think: Your money → Your friend's money

What actually happens: Your bank → App's holding account → Friend's app balance → (eventually) Friend's bank

The app sits in the middle of every transaction, seeing every detail, controlling both ends.

This is fundamentally different from cash (truly peer-to-peer) and cryptocurrency (peer-to-peer via different mechanism). Understanding this helps you evaluate privacy and control trade-offs.

When Payment Apps Make Sense

Good for:

Splitting bills with friends (already on the same app)

Quick small payments where convenience matters

Situations where you trust the app's protections

Watch out for:

Keeping large balances (use a bank instead)

Business transactions (different protections apply)

Assuming "instant" means "final"

Sending to wrong people (hard to reverse)

Key Takeaways

Payment apps are digital IOU systems—they update scores rather than moving money

"Instant" transfers are instant in-app but actual bank movement takes days

Apps profit from fees, float, and data—the service isn't truly free

Balances may not be insured like bank accounts—companies can freeze accounts

All transactions go through a middleman despite feeling peer-to-peer

Convenience comes with trade-offs in privacy, control, and protection

Last updated