Lesson 8: What Happens During Bank Hours

🎧 Lesson Podcast

🎬 Video Overview

What Happens During Bank Hours

Core concept: Traditional banks operate on limited hours, creating a gatekeeper between you and your money that's only available when it's convenient for them.

The 9-5 Gatekeeper

Picture this: It's 8 PM on a Friday. You need to resolve a problem with your account—maybe a fraudulent charge, a transfer that didn't go through, or a question about a large deduction. You call your bank.

"Our business hours are Monday through Friday, 9 AM to 5 PM. Please call back during normal business hours."

Your money doesn't sleep. The economy doesn't stop. But the people who control access to your money decided they'd rather not be bothered on weekends.

This limitation seems archaic in 2024, but it persists because banking infrastructure was built in an era of paper ledgers and physical vaults. Many systems still operate on that schedule, even though the technology could work 24/7.

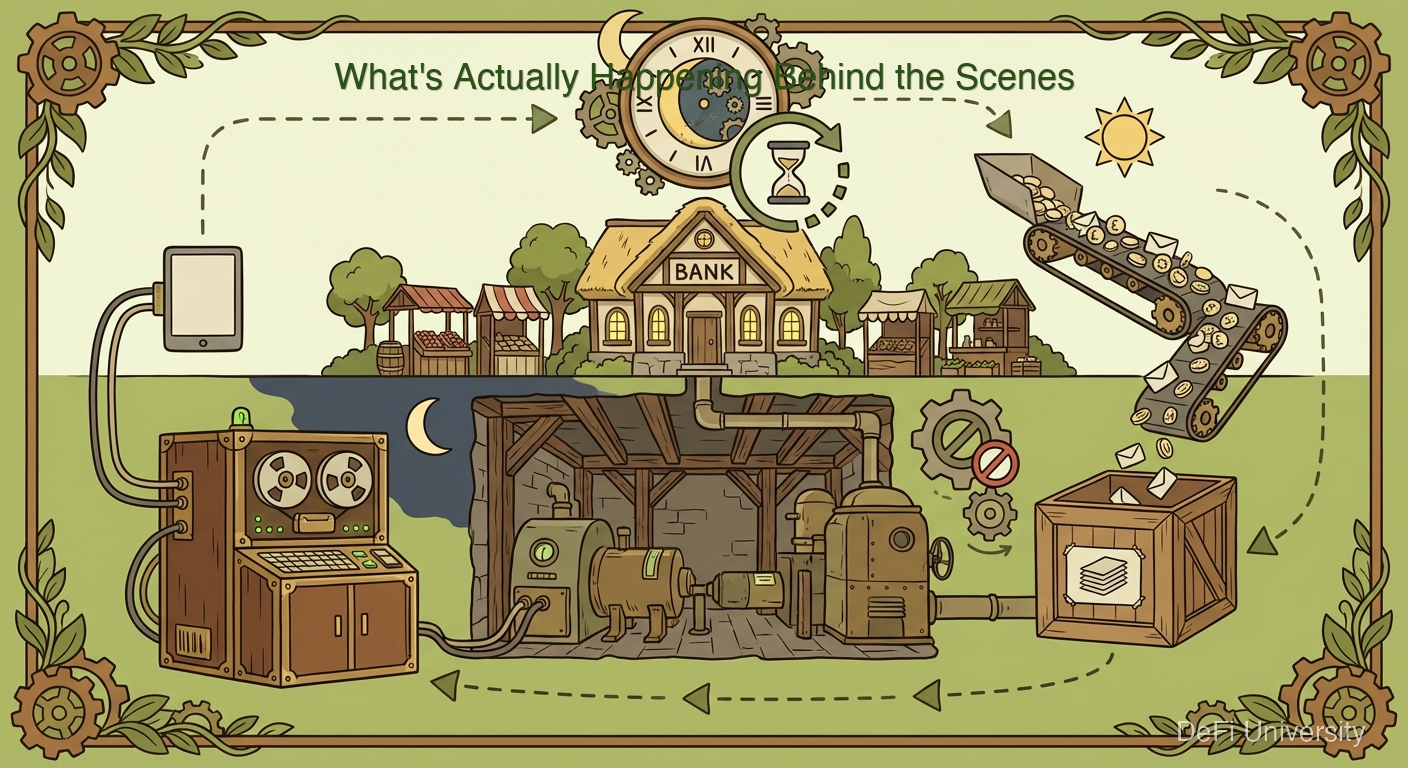

What's Actually Happening Behind the Scenes

Why can't banks just... work all the time? A few reasons:

Legacy Systems

Most major banks run on software built 30-50 years ago. These systems were designed for batch processing—collecting all the day's transactions and processing them together overnight. Changing this requires rebuilding infrastructure that's deeply embedded in everything the bank does.

Settlement Networks

When money moves between banks, it goes through intermediary networks like the Federal Reserve's ACH (Automated Clearing House) system. These networks have historically operated on banking hours. If Bank A needs to send money to Bank B, they batch the request and send it through ACH, which processes it... eventually.

Risk and Reconciliation

Banks need time to verify transactions, catch fraud, and reconcile their books. Processing everything in real-time would require different (expensive) infrastructure. It's cheaper for them to batch things up.

Regulation

Banking is heavily regulated. Changes to systems require approval, testing, and compliance verification. Moving slowly is partly about managing regulatory risk.

The Weekend Freeze

Here's what happens when you "send" money on a Friday night:

Friday 8 PM: You initiate a transfer to a friend.

Friday 8 PM - Monday 8 AM: The transfer sits in a queue. Nothing moves.

Monday morning: Your bank submits the transfer request to the network.

Monday - Wednesday: The request moves through the system, gets processed in batches, and eventually reaches your friend's bank.

Wednesday or Thursday: The money finally appears in your friend's account.

Your friend sees the money Tuesday or Wednesday. You thought it happened Friday. Neither of you knows it was actually sitting in limbo for days.

During this time, the banks might be earning interest on your "in-transit" money. It's called "float," and it's profitable for them.

What "Available" vs. "Posted" Really Means

Check your bank account and you might see two numbers:

Available balance: What the bank will let you spend

Posted balance: What's actually finalized in your account

These often differ because transactions haven't fully settled. You might see $1,000 available but $800 posted because a $200 transaction is "pending."

This creates confusion and sometimes leads to overdrafts. You thought you had the money—the app even showed it—but technically you didn't.

International Gets Worse

Domestic banking is slow. International is glacial.

Sending money abroad involves:

Your bank

An intermediary bank (or several)

Currency conversion

The recipient's country's banking system

The recipient's bank

Each step adds time and fees. International wire transfers commonly take 3-5 business days and can cost $40-80 in combined fees.

For migrant workers sending money home to families, these delays and costs are a significant burden. A worker sending $200 home might lose $15-30 to fees, and the family won't see it for a week.

Why This Matters

The limited hours and slow speeds of traditional banking have real consequences:

For individuals: Bills don't wait for banking hours. Rent is due on the 1st even if your paycheck is "processing."

For small businesses: Cash flow depends on fast payments. Waiting days for customer payments to clear creates real problems.

For the unbanked: Limited hours make banking even harder for people who work multiple jobs during bank hours.

For global commerce: The friction of international transfers inhibits economic activity.

Understanding these limitations helps explain why alternatives are attractive. Cryptocurrency networks operate 24/7, 365 days a year. Transfers settle in minutes or hours, not days. Whether this trade-off is worth the other differences depends on your needs—but the comparison is worth understanding.

Key Takeaways

Banks operate on limited hours—9-5 weekdays for most customer service and processing

Legacy systems and settlement networks create delays even when technology could be faster

Weekend transfers don't actually move until Monday, despite instant appearance

"Available" and "posted" balances differ because transactions take time to settle

International transfers are slower and more expensive due to multiple intermediaries

24/7 alternatives exist and operate on fundamentally different infrastructure

Last updated