Lesson 11: Why Transfers Take Days

🎧 Lesson Podcast

🎬 Video Overview

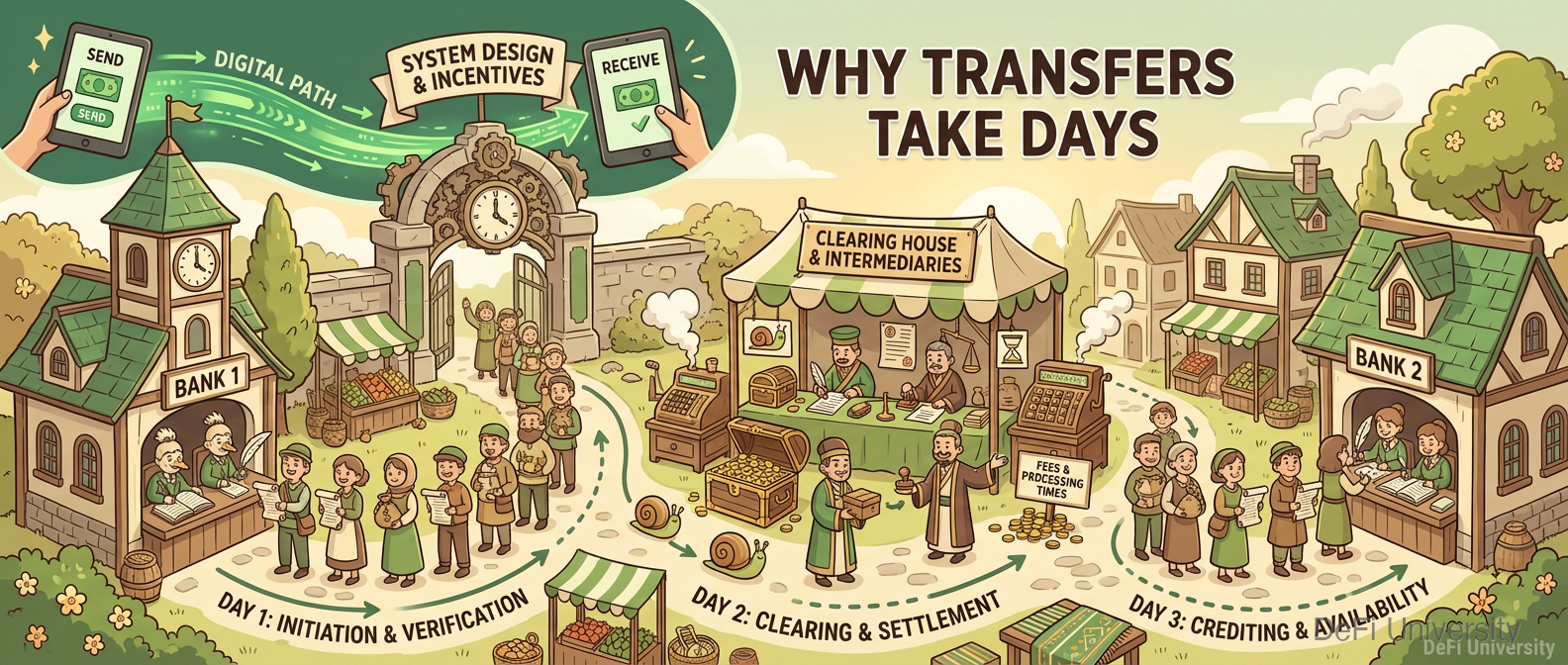

Why Transfers Take Days

Core concept: Bank transfers take days not because of technology limitations, but because of how the system was designed and the incentives of those running it.

Relay Race vs. Instant Messaging

When you send an instant message, information travels from your phone to a server to your friend's phone in milliseconds. The technology for instant communication has existed for decades.

So why does sending money feel like running a relay race with rest stops?

Imagine you need to pass a baton from New York to Los Angeles. Instead of flying directly, you:

Drive to a regional hub

Wait for morning

Hand off to someone going west

They drive to another hub

Wait for morning

Hand off again

Continue until Los Angeles

Each "wait for morning" is equivalent to what banks call "batch processing." They collect all the day's transactions, wait until the end of business, then process them in batches overnight.

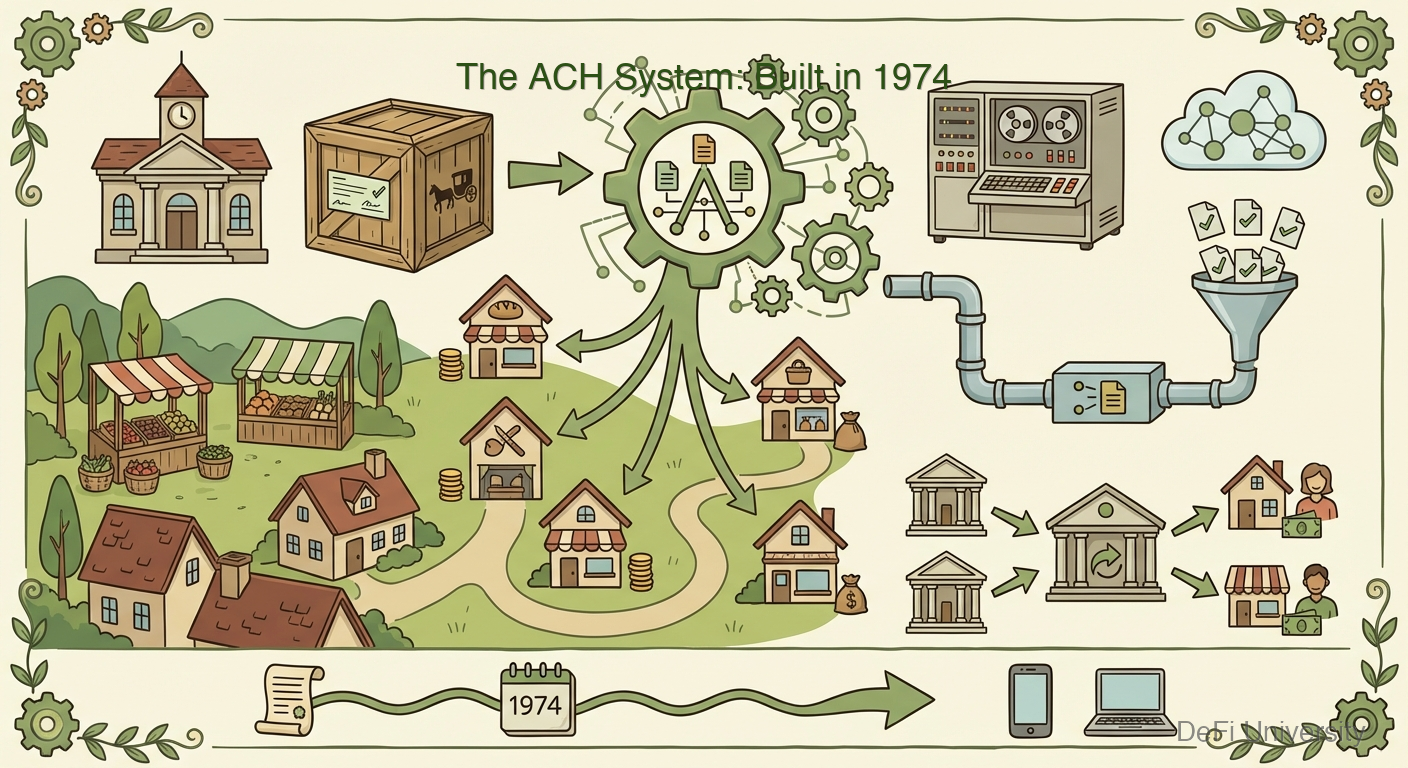

The ACH System: Built in 1974

Most bank transfers in the US go through ACH—the Automated Clearing House. It was created in 1974 to replace physical check transport between banks.

In 1974, batch processing made sense. Computers were expensive, networks were slow, and processing transactions individually was impractical. Batching everything overnight was efficient.

The problem? The system was never fundamentally redesigned. Modern additions have been bolted on, but the core still operates like it's 1974—in a world of smartphones and instant communication.

The Float Profit

Here's an uncomfortable truth: delays are profitable.

When money is "in transit," it sits somewhere. That somewhere is typically earning interest. The longer the delay, the more interest earned.

Example: Your employer sends payroll on Friday. You don't receive it until Tuesday. That's 4 days your money sits in limbo. Multiply this by millions of transactions and billions of dollars—that float generates significant income for the institutions holding it.

If banks could move money instantly (they can—see Zelle, FedNow), they'd lose this float revenue. The technical capability exists; the incentive to use it is complicated.

What Each Delay Step Does

Breaking down a typical bank transfer:

Day 0 (you initiate): Your bank receives the request and queues it for the next batch processing window.

Day 1 (batch processing): Overnight, your bank sends the request to the ACH network. The network sorts millions of transactions and routes them to receiving banks.

Day 1-2 (receiving bank processing): The receiving bank gets the instruction, verifies details, and queues the credit for their customer.

Day 2-3 (availability): The receiving bank may hold funds for "risk review" before making them available.

Each step includes legitimate fraud prevention... and opportunities to hold money longer.

International Is Even Slower

Cross-border transfers add layers:

Correspondent Banking: Your bank probably doesn't have a direct relationship with a bank in Singapore. So your money goes: Your bank → US correspondent bank → International correspondent bank → Singapore correspondent bank → Recipient's bank.

Each hop takes time and costs money.

Different Systems: Every country has different banking infrastructure, regulations, and processing schedules. Coordinating across these adds friction.

Compliance Checks: International transfers face anti-money-laundering scrutiny at multiple points, adding delays.

Currency Conversion: Someone has to handle the exchange rate, usually at a markup.

This is why sending money abroad takes 3-5 days and costs $30-50. The complexity is real—but so is the profit extracted at each step.

Faster Alternatives Exist

The technology for faster transfers has existed for years:

RTP (Real-Time Payments): Launched 2017, enables instant bank-to-bank transfers 24/7. Adoption is still limited.

FedNow: Federal Reserve's instant payment system launched 2023. Slowly being adopted by banks.

Zelle: Near-instant between participating banks because they've agreed to settle among themselves.

The technology is there. The question is whether institutions have incentives to adopt it broadly—and whether they'll charge premium fees for the privilege of speed.

Why This Matters for Crypto

Understanding banking slowness helps you understand crypto's appeal:

Bitcoin settles in 10-60 minutes, 24/7

Ethereum settles in seconds to minutes

Stablecoins move value across borders without correspondent banks

Cryptocurrency isn't just about philosophy—for many use cases, it's simply faster and cheaper infrastructure for moving value.

Whether that matters depends on your needs. If you're splitting dinner with friends, waiting 3 days is irrelevant. If you're sending money to family overseas during an emergency, those days matter enormously.

Key Takeaways

Bank transfers use 1974-era batch processing—designed for a different technological era

Float is profitable—delays generate interest income for those holding "in-transit" money

Each step adds legitimate and opportunistic delays—fraud prevention and profit extraction blend together

International adds correspondent banks—each hop takes time and money

Faster systems exist but adoption is slow—RTP, FedNow, and Zelle prove speed is technically possible

Crypto offers different speed/cost trade-offs—understanding why helps evaluate alternatives

Last updated