Lesson 5: What Banks Actually Do

🎧 Lesson Podcast

🎬 Video Overview

What Banks Actually Do

Core concept: Banks are middlemen that hold your money, move your money, and lend your money to others—all while charging fees for the service.

The Middleman at the Swap Meet

Imagine a giant swap meet where thousands of people want to trade with each other. Instead of everyone finding their own trading partners, a guy named Bob sets up a booth in the middle.

"Give me your stuff," Bob says. "I'll keep it safe. When you want to trade with someone, just tell me, and I'll handle the exchange. Oh, and if you don't need your stuff right now, I'll rent it out to people who do and share some of the profit with you."

That's essentially what a bank does. Bob is your bank.

The system has advantages: you don't have to carry your valuables around, you don't have to find trading partners, and you can earn a little extra from stuff you're not using. The disadvantage: Bob takes a cut of everything, and you're trusting Bob with your stuff.

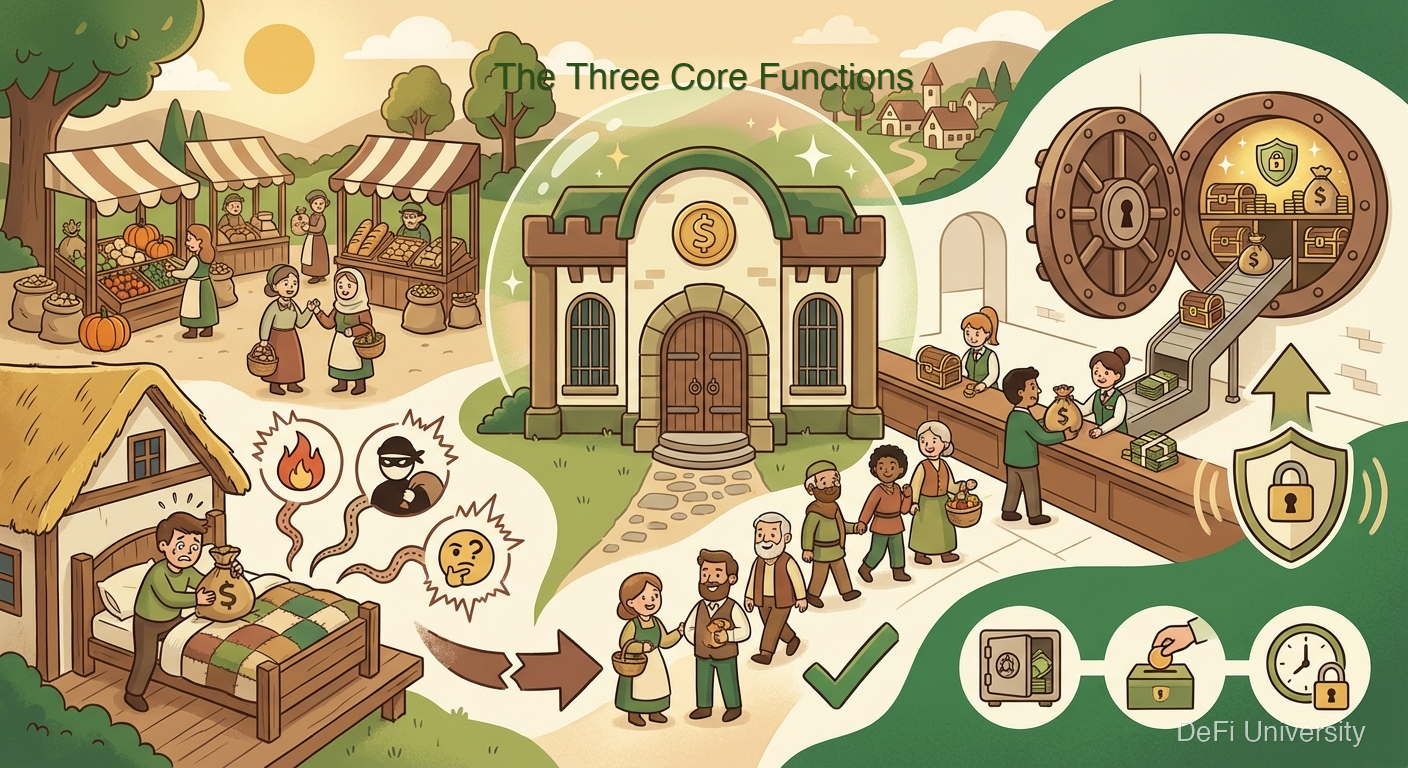

The Three Core Functions

Banks serve three main purposes:

1. Safekeeping (Deposits)

Banks hold your money so you don't have to. Instead of keeping cash under your mattress (risky—fire, theft, forgetfulness), you keep it in a bank account (less risky—insured, trackable, accessible).

When you "deposit" money, you're actually lending it to the bank. They promise to give it back when you ask, but in the meantime, they use it for other things.

2. Payments (Transfers)

Banks move money between accounts. When your employer pays you, when you pay rent, when you buy something online—banks are coordinating these transfers behind the scenes.

Before digital banking, this meant physically moving checks and records between bank branches. Now it's mostly database updates, but the process is still surprisingly slow (more on that in later lessons).

3. Lending (Credit)

Banks take the money deposited by many people and lend it to others who need money now—for houses, cars, businesses, emergencies. The bank charges borrowers interest and pays depositors a smaller interest rate. The difference is profit.

This is how banks make most of their money: they pay you 0.5% interest on your savings while charging someone else 7% for a car loan. That spread is their business model.

The Magic Trick: Fractional Reserve

Here's something that surprises most people: banks don't keep all your money sitting in a vault.

If you deposit $1,000, the bank keeps maybe $100 on hand and lends out $900 to someone else. This is called "fractional reserve banking"—they only keep a fraction of deposits as reserves.

This works because most people don't withdraw all their money at once. As long as withdrawals and deposits roughly balance out, the bank can keep operating.

But if everyone suddenly wants their money back at the same time (called a "bank run"), the bank doesn't have it. This is why bank failures happen and why governments created deposit insurance—to prevent panic withdrawals.

What You Get (and What You Pay)

Banks provide genuine value:

Security: Your money is safer than cash at home

Convenience: Easy payments, ATMs, online access

Credit access: Ability to borrow when needed

Insurance: Government protection (up to limits) if the bank fails

But you pay for these services:

Low interest on deposits: Your savings earn far less than inflation

Fees: Monthly maintenance, overdraft, ATM, wire transfer fees

Your time: Applying for accounts, waiting for approvals, following their rules

Your data: Banks know everything about your financial life

The question isn't whether banks provide value—they do. The question is whether the trade-offs are worth it for your situation, and whether better alternatives exist.

The Gatekeeper Role

Banks also serve as gatekeepers to the financial system. To open an account, you typically need:

Government ID

Social Security number or equivalent

Physical address

Clean enough financial history

This keeps out some bad actors but also excludes people who lack documentation—immigrants, homeless individuals, people in developing countries without robust ID systems.

Globally, about 1.4 billion adults lack access to basic banking. They're "unbanked"—stuck using cash, check-cashing services, or informal arrangements. Understanding this helps explain why alternatives to traditional banking matter.

Key Takeaways

Banks are middlemen that safeguard money, facilitate payments, and make loans

Your deposit is a loan to the bank—they use it to lend to others

Fractional reserve means banks don't keep all deposits on hand

Banks profit from the spread between what they pay depositors and charge borrowers

Banks are gatekeepers—you need their approval to access the financial system

Billions of people are unbanked because they can't meet bank requirements

Last updated